Every day, 10,000 more baby boomers hit retirement age, according to the Pew Research Center. By 2030, 18 percent of the nation will be 65 or older.

Every day, 10,000 more baby boomers hit retirement age, according to the Pew Research Center. By 2030, 18 percent of the nation will be 65 or older.

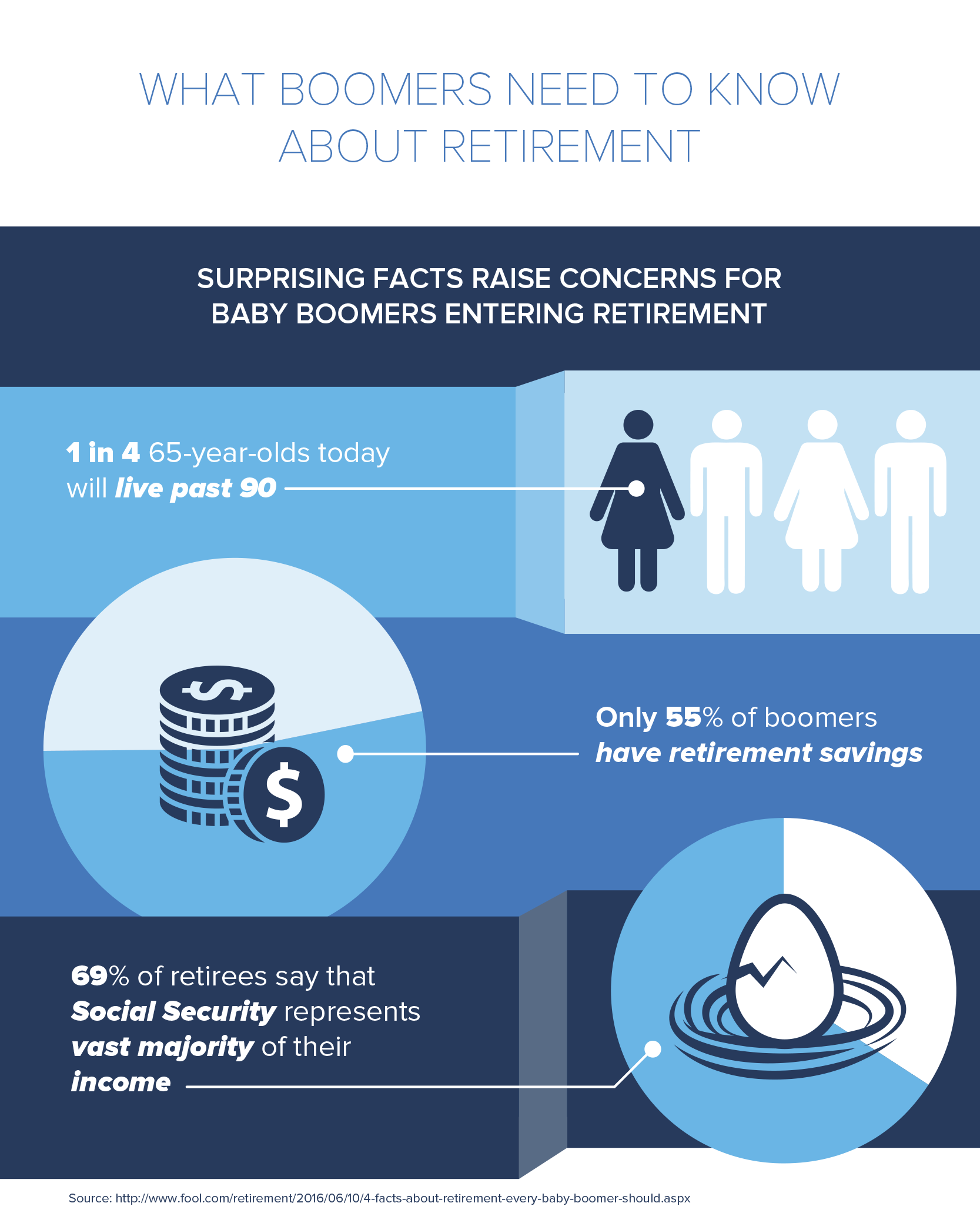

As boomers depart the workforce, though, they could encounter a few challenges. Here are four things boomers need to know as they head into their non-working years:

- You’ll probably live longer than you think. According to the Social Security Administration, a 65-year-old man today can expect to live, on average, to age 84, and the average 65-year-old female lives to just over age 86. Many more live longer: one in four 65 year olds today will live past 90. One in 10 will live past 95. That means many boomers will need to support a retirement of 20 to 30 years.

- You might need to save more. According to a report from the Insured Retirement Institute, only 55 percent of boomers have retirement savings. Among those who have saved, nearly half—42 percent—have less than $100,000 put away. A retirement nest egg of $100,000 would allow for an annual income of just $7,000 over a 20-year retirement period.

- Social Security isn’t enough. Many retirees rely heavily on Social Security: 22 percent of married couples and 47 percent of unmarried individuals say it represents 90 percent or more of their income. But the average monthly benefit for a retiree in 2016 is just $1,341, or $16,092 a year. That’s often not enough to take care of living expenses or rising health care costs.

- Retirement savings worries are common. According to the IRI study, less than a quarter of boomers—24 percent—are confident their retirement savings will last through retirement. That’s the lowest confidence level the IRI has seen since it launched the study in 2011.

It’s not all bad news, though. Boomers on the verge of retiring can take steps now to better position themselves for their non-working years. Catch-up contribution rules allow anyone 50 and older to contribute more to their 401(k) and IRA accounts. Boomers can also postpone retirement, gaining a few more years of working income.

And when possible, boomers should consider delaying claiming Social Security benefits. While full retirement age is 66 or 67, depending on year of birth, each year benefits are postponed—until age 70—results in an 8 percent increase in benefits. That increase remains in effect for as long as the individual claims benefits.